Cannabis retail has transformed faster in the last five years than in the previous twenty. What used to be driven by marketplaces and directory sites is now driven by local SEO, Google Maps dominance, CRM automation, and owned ecommerce channels. For dispensaries, this shift has created massive opportunity — and massive risk for those who haven’t kept up.

Below is the full evolution of the cannabis ecommerce landscape, and what operators must do to stay competitive in 2025 and beyond.

Cannabis Retail Has Changed More in the Last Five Years Than in the Previous Twenty

A sudden leap forward — not a slow evolution

From 2005–2020, cannabis retail moved slowly: list on Weedmaps, open the doors, hope customers show up.

But 2020–2025 triggered a complete acceleration:

- Delivery took off in mature markets

- Google Maps eclipsed directory platforms

- Ecommerce menus became standard

- CRM automations started driving 40–60% of repeat purchases

- Operators began competing on systems, not hype

Cannabis retail jumped from a “walk-in novelty shop” model to a fully digital, data-driven retail ecosystem — almost overnight.

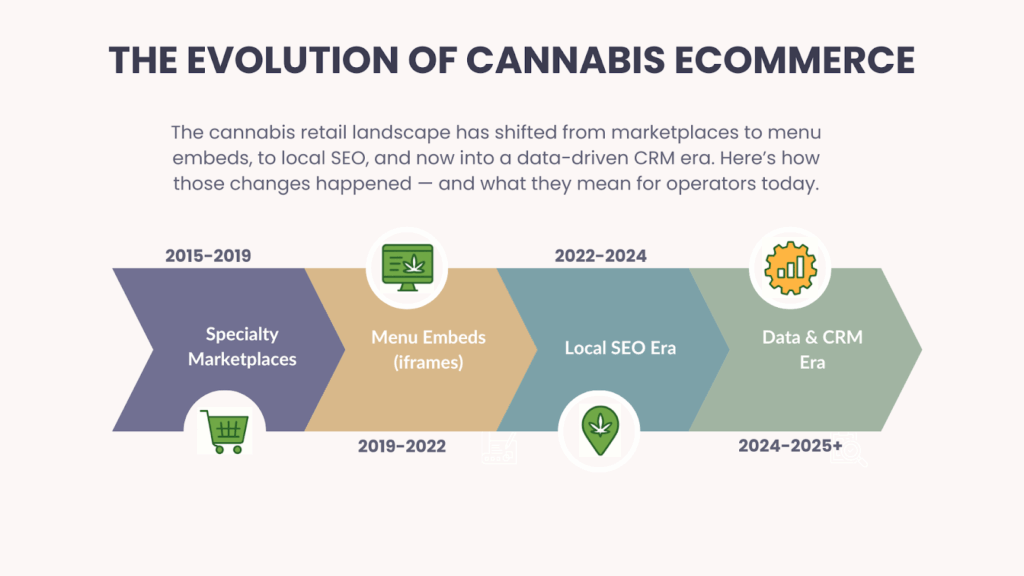

Era #1 (2015–2019): The Marketplace Era — Weedmaps, Leafly, and the Discovery Monopoly

Why marketplaces dominated this era

In early legal markets, customers didn’t know:

- who was licensed

- who carried what

- who delivered

- what was in stock

Marketplaces solved that. One hub, all shops. For years, that was enough.

What made Weedmaps + Leafly inevitable early on

They became the “Amazon of cannabis” because:

- Google was inconsistent about cannabis listings

- Operators lacked websites

- Delivery rules were unclear

- Products varied wildly

- Consumers had no loyalty

So the path became: Find store → pick product → place order on Weedmaps → pick up in-store.

The cracks that formed in the model

By 2019, operators realized:

- Marketplace customers are loyal to the platform, not the brand

- Data wasn’t portable

- Marketing spend wasn’t trackable

- Pricing was a race to the bottom

- It inflated “demand” for brands that weren’t actually winning in-store

Operators wanted out — but didn’t yet have alternatives.By 2019, operators realized:

- Marketplace customers are loyal to the platform, not the brand

- Data wasn’t portable

- Marketing spend wasn’t trackable

- Pricing was a race to the bottom

- It inflated “demand” for brands that weren’t actually winning in-store

Operators wanted out — but didn’t yet have alternatives.

Era #2 (2019–2022): The Menu Embedding Era — Jane, Dutchie, and First-Gen Dispensary Ecommerce

The rise of native menus

Suddenly, dispensaries had:

- websites

- licensed ecommerce

- real-time menus

- order-ahead integration

Jane, Dutchie, I Heart Jane, and others built infrastructure that finally allowed operators to own their ecommerce experience.

Why this era was necessary — but flawed

These menus solved availability, compliance, and order flow. But they did not solve discovery.

Menu embedding without SEO = wasted potential

Most operators simply embed an iframe or Dutchie/Jane page, which:

- carries zero SEO value

- drives zero organic traffic

- creates a dead end funnel

Operators thought: “We have ecommerce now — problem solved.”

But the actual demand engine was forming somewhere else…

Era #3 (2022–2024): The Local SEO & Google Maps Era

Why Google now dominates cannabis discovery

Search behavior changed dramatically:

2024 Search Data Signals

- “dispensary near me” → up 5× year-over-year

- “cannabis delivery near me” → up 4–6× in legal states

- Clicks on Google Maps locations surpassed clicks on menu platforms

- 60–70% of dispensary website visits originate from branded or local-intent Google queries

Google — not Weedmaps — became the starting point.

Data from search behavior shifts

In 2018, Weedmaps/Leafly drove ~60% of cannabis online discovery. By 2024, it dropped to approx 15–20% (varies by state).

Google took the rest.

How dispensaries adapted (or didn’t)

Operators who thrived:

- cleaned up NAP consistency

- mapped and optimized all locations

- built category + product SEO pages

- drove reviews intentionally

- tied Maps traffic to CRM

Those who didn’t — vanished.

Era #4 (2024–2025): The CRM, Data & Attribution Era

Why data became non-negotiable

Modern cannabis ecommerce = data-driven retail.

The highest-performing operators now:

- track click → cart → sale

- segment customers

- automate SMS/email

- measure ROAS by channel

- use product affinity models

- optimize LTV by cohort

How lack of integrations cripples operators

Dispensary tech stacks are still fragmented.

But the cost of NOT integrating is massive:

- wasted marketing budget

- no view of which channels convert

- poor reorder logic

- blind promotional strategy

The new growth engine: owned channels + retention

Today’s winners are those who:

- own customer data

- build loyalty funnels

- run automated nurture

- retain their top 20% of customers

- grow via targeted promos, not discounts

What This Evolution Means for Operators in 2025

The skills and systems required to win

Winning dispensaries now run on:

- retail systems

- data literacy

- sales accountability

- customer experience mapping

- SEO + Maps strategy

What operators must unlearn

Old belief: “Weedmaps handles everything.”

Reality: It handles almost nothing today.

Old belief: “Budtenders don’t need sales training.”

Reality: They absolutely do.

Why training & performance matter more now

Customers choose based on:

- convenience

- speed

- staff confidence

- consistency

Those depend on training and operations, not marketing.

The Modern Cannabis Tech Stack (2025)

POS

Sweed, BioTrack, Dutchie POS, Treez, Flourish, Greenline.

CRM & Loyalty

AlpineIQ, Springbig, HappyCabbage, Trees.

Ecommerce

Sweed, Dutchie, Jane, Tymber, Dispense.

Analytics

Headset, Jane API, custom dashboards, or AI-led BI.

Training Systems

Straight Fire (homepage), Bridge, Trainual, or custom SOP ecosystems.

Where Cannabis Shoppers Actually Start Their Search in 2025

Updated funnel

- Google Maps

- Branded website

- Ecommerce

- Pickup

- CRM remarketing

Differences by state

- Florida → loyal shoppers + Maps discovery

- California → ecommerce-first

- Michigan → deal seeking + delivery

- Pennsylvania → loyalty funnels

Why Google Maps ranking is the new battleground

Maps = intent + locality. It’s the highest “purchase-ready” traffic in cannabis.

Why Marketplaces Still Matter — But Aren’t Your Growth Engine

What marketplaces are good for

- tourists

- new customers

- visibility

Where they fail

- no retention

- no data

- no brand loyalty

- no differentiation

Why operators who rely on them lose

They acquire the customer — not you. You pay rent on your own traffic.

How to Prepare Your Dispensary for the Next Era of Ecommerce

The operator checklist

- Fix Maps + SEO

- Own your ecommerce

- Integrate CRM

- Train your people

- Build performance culture

Marketing upgrades needed

- Content-rich ecommerce

- Category pages

- Product education

- Google Merchant Center (where legal)

- Review velocity

Training/operations upgrades needed

- Sales scripts

- Cannabis literacy

- Consultative selling

- Internal SOP systems

- Manager cadence

Ready to Modernize Your Dispensary’s Ecommerce?

Work with Straight Fire to upgrade your retail systems

We help dispensaries build modern ecommerce funnels, improve sales performance, and replace operational chaos with real systems.

→ Explore Cannabis Consulting (/cannabis-consulting)

→ Dispensary Training Program (/dispensary-training)

Cannabis E-Commerce FAQs

Is Weedmaps still relevant in 2025?

Yes — but only for discovery. It is not a long-term growth engine or retention channel.

Where do customers start their cannabis search now?

Most begin on Google Maps or branded local searches.

What’s the best ecommerce setup for dispensaries?

A SEO-optimized ecommerce website with an integrated menu, CRM, and analytics.

Do dispensaries still need SEO?

Absolutely — SEO + Maps optimization drives the highest-intent traffic in cannabis.

What’s the future of cannabis ecommerce?

Owned data, local search domination, loyalty funnels, and retail-powered training.